The 50/30/20 Rule: A Data-Driven Approach to Simple Budgeting

Discover the mathematical framework behind the most popular budgeting strategy and learn how to allocate your income for maximum financial impact.

The 50/30/20 Rule: A Data-Driven Approach to Simple Budgeting

Budgeting is often perceived as a restrictive practice, but at its core, it is a tool for resource optimization. One of the most effective and mathematically sound frameworks for personal finance is the 50/30/20 rule.

This guideline provides a clear structure for allocating your after-tax income, ensuring that you cover your essentials while consistently building wealth for the future.

The Mathematical Framework

The rule breaks down your monthly take-home pay into three distinct categories:

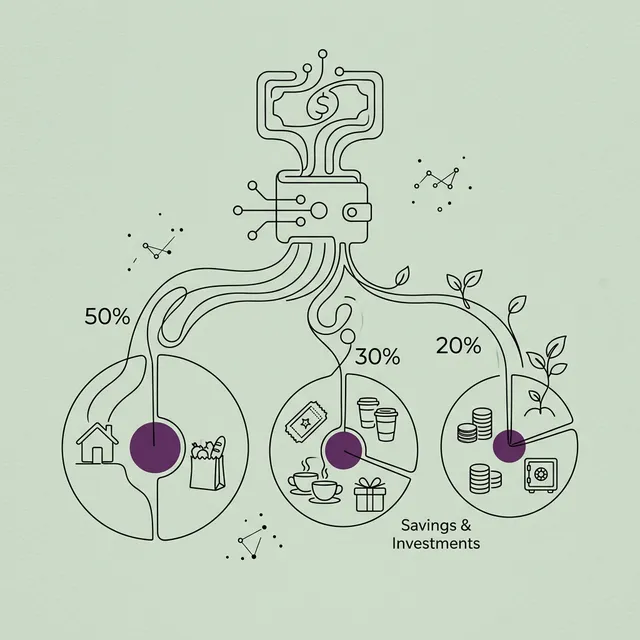

50% for Needs

Half of your income should be reserved for absolute necessities. These are the non-negotiable costs required for survival and basic functioning.

- Housing: Rent or mortgage payments.

- Utilities: Electricity, water, and basic internet.

- Groceries: Essential food items (excluding dining out).

- Insurance: Health, auto, and life insurance premiums.

- Minimum Debt Payments: The baseline amount required to stay current on loans.

30% for Wants

This category represents your lifestyle choices. While technically optional, these expenses contribute to your quality of life and personal fulfillment.

- Entertainment: Streaming services, movies, and hobbies.

- Dining Out: Restaurants, coffee shops, and takeout.

- Shopping: Non-essential clothing and electronics.

- Travel: Vacations and weekend trips.

20% for Savings and Extra Debt Repayment

This is the “wealth-building” slice of the pie. This 20% should be prioritized to ensure long-term financial independence.

- Emergency Fund: Building a safety net.

- Retirement: Contributions to 401(k) or IRA accounts.

- Extra Debt Payoff: Payments above the minimum to reduce principal faster.

Why It Works

The 50/30/20 rule is popular among financial educators because it solves the “analysis paralysis” common with granular budgeting. Instead of tracking dozens of categories, you only need to manage three high-level buckets.

From an SEO perspective, this method is highly sought after because it remains relevant regardless of income level. Whether you are earning $40,000 or $140,000, the percentage-based approach scales with your lifestyle.

Optimizing Your Allocation

If you find that your “Needs” exceed 50%—a common challenge in high-cost-of-living areas—the strategy is to reduce the “Wants” category until you can lower your fixed costs.

To see how your current spending aligns with this model, you can use our Budget Calculator to input your income and expenses. It will help you visualize exactly where your percentages sit today.

Taking Action

The first step is to calculate your net income (your pay after taxes and 401k contributions are removed). Once you have that number, multiply it by 0.50, 0.30, and 0.20 to find your targets.

If you find that your 20% savings goal is currently going toward high-interest debt, consider analyzing your payoff strategy. Our Invest vs Debt Tool can help you decide if you should focus that 20% on your credit cards or your brokerage account.

This guide is for educational purposes only. Always consult with a certified financial professional for specific advice regarding your unique financial situation.

Disclaimer

This analysis is for educational purposes only and does not constitute financial advice. The models presented are projections based on historical data and specific assumptions that may not apply to your unique situation. Always consult with a certified financial professional.

Content on StashPlanner is created with the assistance of Artificial Intelligence. While we fact-check against high-authority sources, AI can occasionally hallucinate or get details wrong. Please use this content as a starting point and always conduct your own due diligence.